Mike Simonsen Economic Presentation

This past week, Alyssa and I visited South Lake Tahoe and attended the Compass NorCal Tahoe Economic Summit alongside 315 other Compass agents. It was among the coolest and most welcoming conferences we've attended and we sincerely appreciate the connections we made with other Compass agents and the time we spent together sharing our respective wins and learning experiences from the past year.

One of the highlights of the Summit was Mike Simonsen's overview of the current economic climate and what it could mean for the next 6 to 24 months. Here is a recap of his slide deck and my commentary on the valuable context Mike provided.

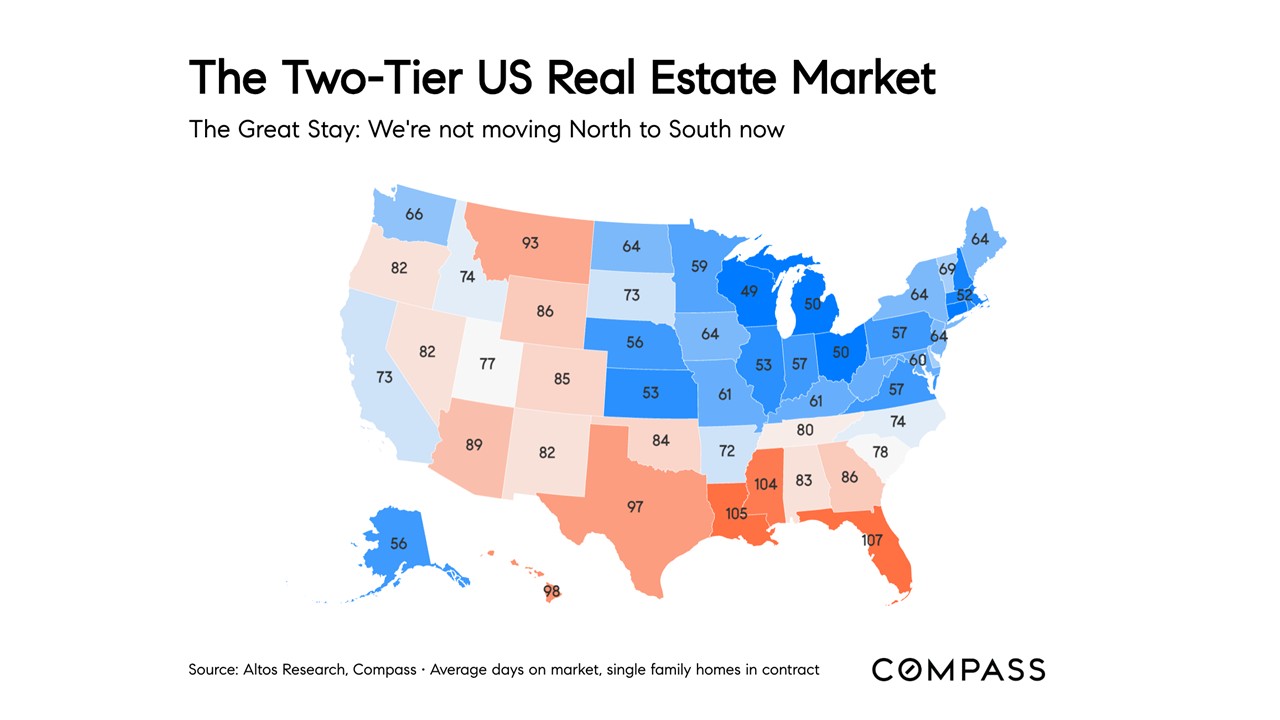

Slide 1

In Mike's first slide, he shared that this heatmap of the United States illustrates the tale of two markets: one in which the Northeast, Midwest, and West Coast have inventory that is still transacting with a reasonable pace (70 days on market and fewer. And a second, in which the Sunbelt states are experiencing more inventory and longer listing periods (70 to 107 average days on market). Mike commented that this is substantially influenced by the massive increase and prices and the significant number of homeowners moving to the Sunbelt during the Covid years.

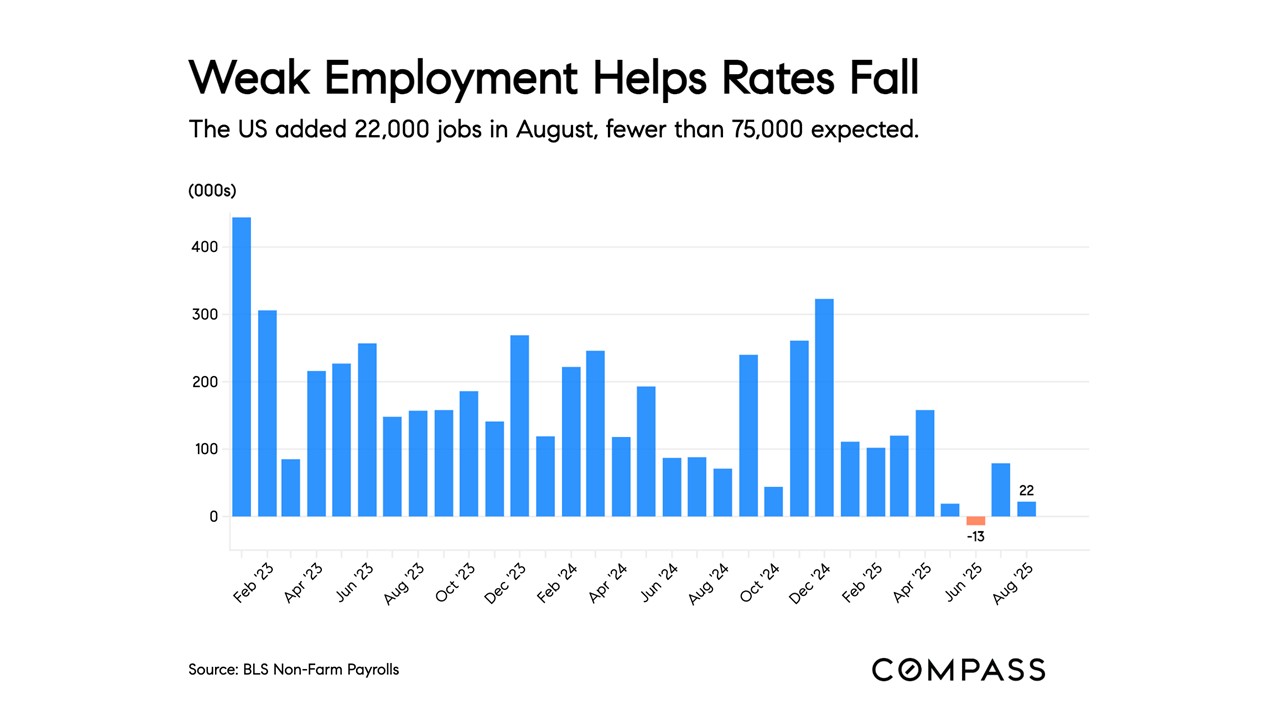

Slide 2

One of Mike's most valuable suggested talking points is, when someone asks him, "what is going to happen with interest rates?" He responds, "I don't know whether they will go up or down, but I can tell you what will happen if interest rates go down." Having said this, Mike indicated through this slide that when the US added fewer new jobs than expected, interest rates have historically gone down.

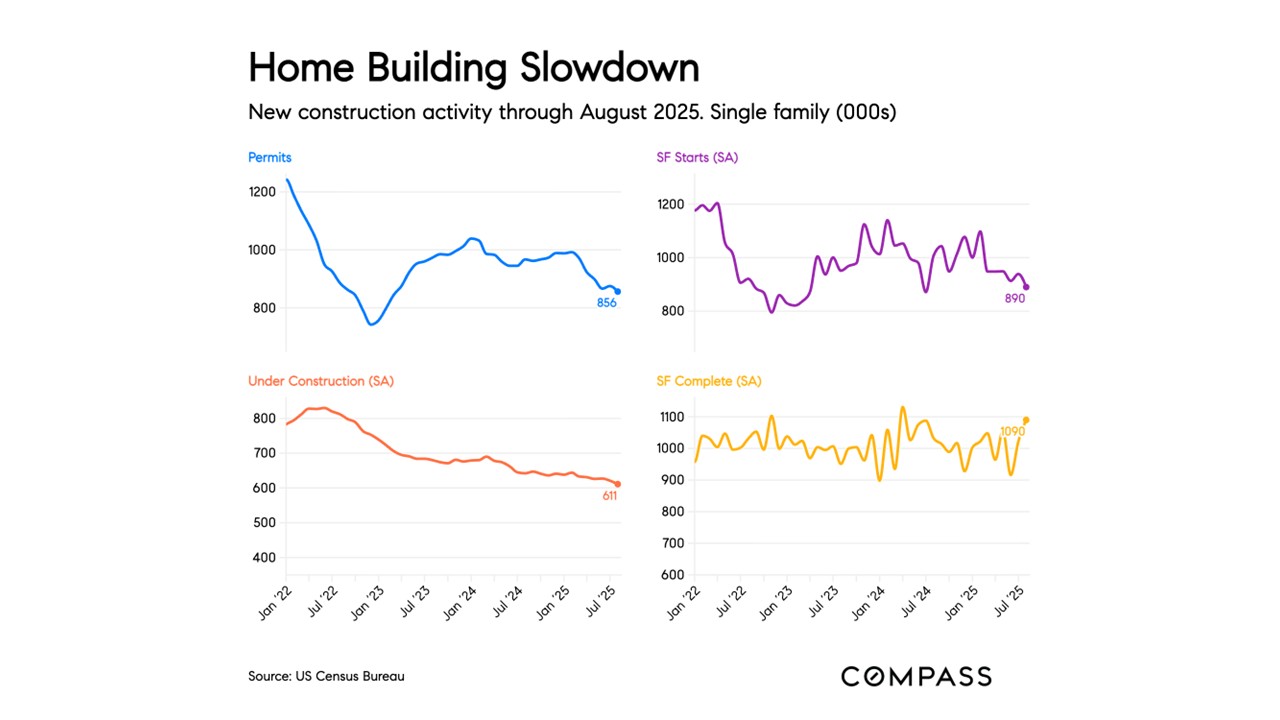

Slide 3

From my perspective, this slide is one of the most impactful in terms of what prices will do for existing homes. These four charts illustrate that the number of new construction home starts are notable down over the last 3 years. This can take a year or two to materialize, but because new construction takes years in planning and permitting, the most likely outcome from the decline in permits and starts will be fewer new construction homes available for sale, which will increase demand for existing homes. If interest rates align, as illustrated later in the presentation, this could make for another period of rapid home price appreciation.

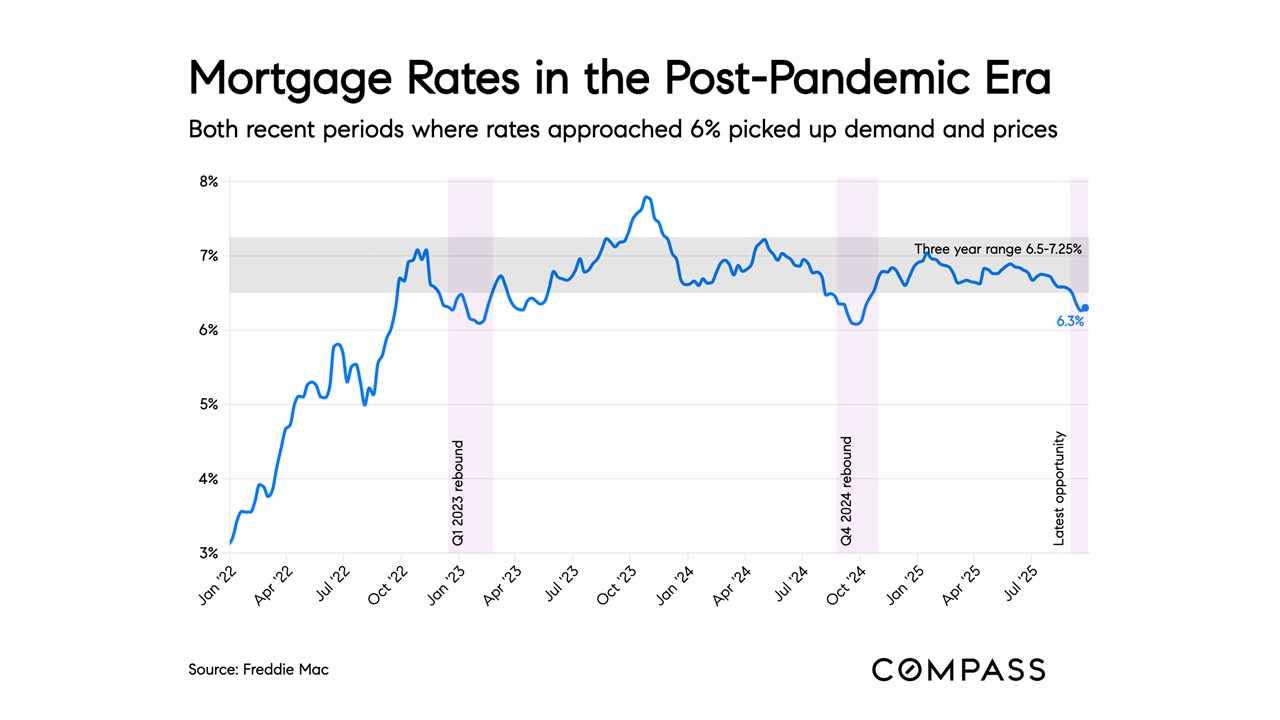

Slide 4

This is the first of two slides (second one is slide 12) that illustrate what will most likely happen if interest rates fall below 6%. In this slide, Mike demonstrated that this is the third time since mortgage rates climbed post-covid that rates have approached 6%. In this two other times when rates have approached 3%, we have experienced an uptick in prices because the cost of homeownership is slightly lower from the lower mortgage rates, so more buyers enter the market.

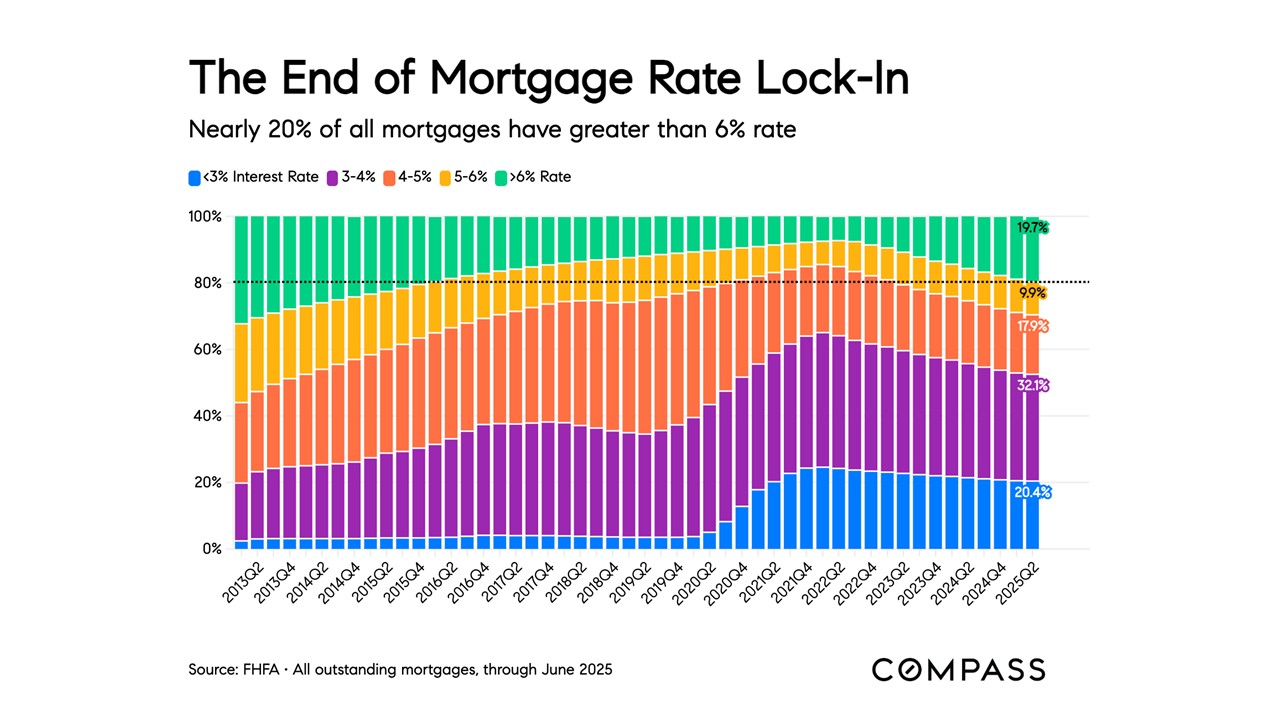

Slide 5

Initially, only 40% own homeowners have a mortgage on their home. This slide illustrates that ~20% of the 40% of mortgage holders now have rates above 6%. Therefore, if rates fall below 6%, there will be more motivation for buyers to transact into a new home purchase and lower their mortgage payment (if the purchase price is the same as their prior home).

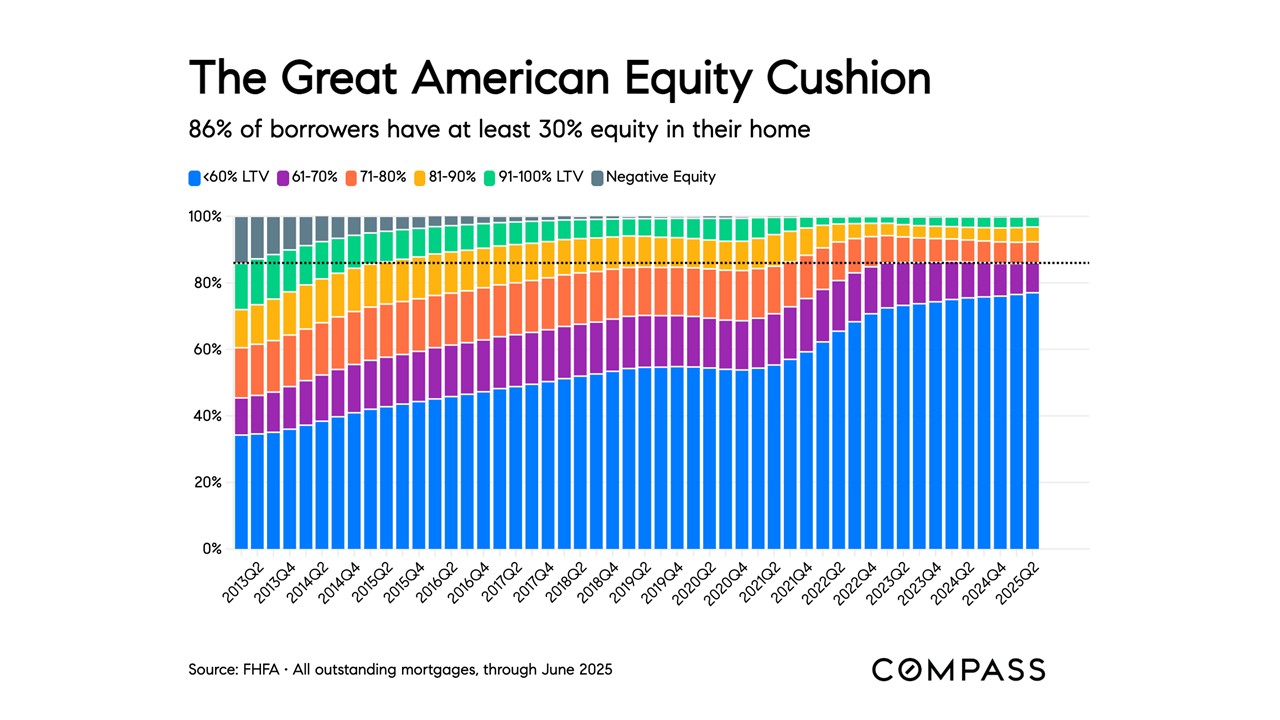

Slide 6

This slide demonstrates that tremendous equity US homeowners have in their homes. Again, it's important to note that only 40% of homeowners have a mortgage. So, of that 40% who have less than 100% equity, 86% of borrowers have more than 30% equity in their homes. This is a good indication that homeowners are most likely not going to be in a distressed state and they can choose to sell at their convenience.

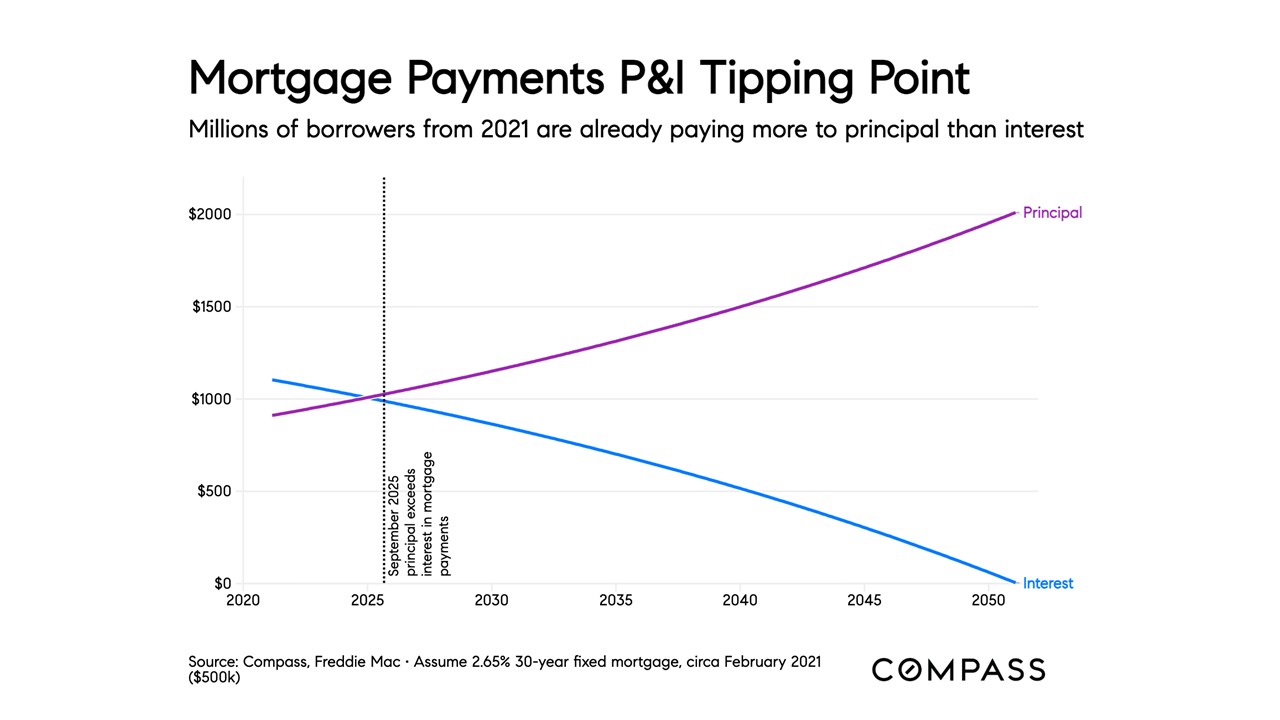

Slide 7

This slide illustrates that homeowners with a sub-3% interest rate are already paying more toward their equity than interest with every monthly payment. Looking forward, this means that more and more homeowners will have a solid amount of equity in their property reducing the number of instances where a homeowner needs to sell for financial reasons.

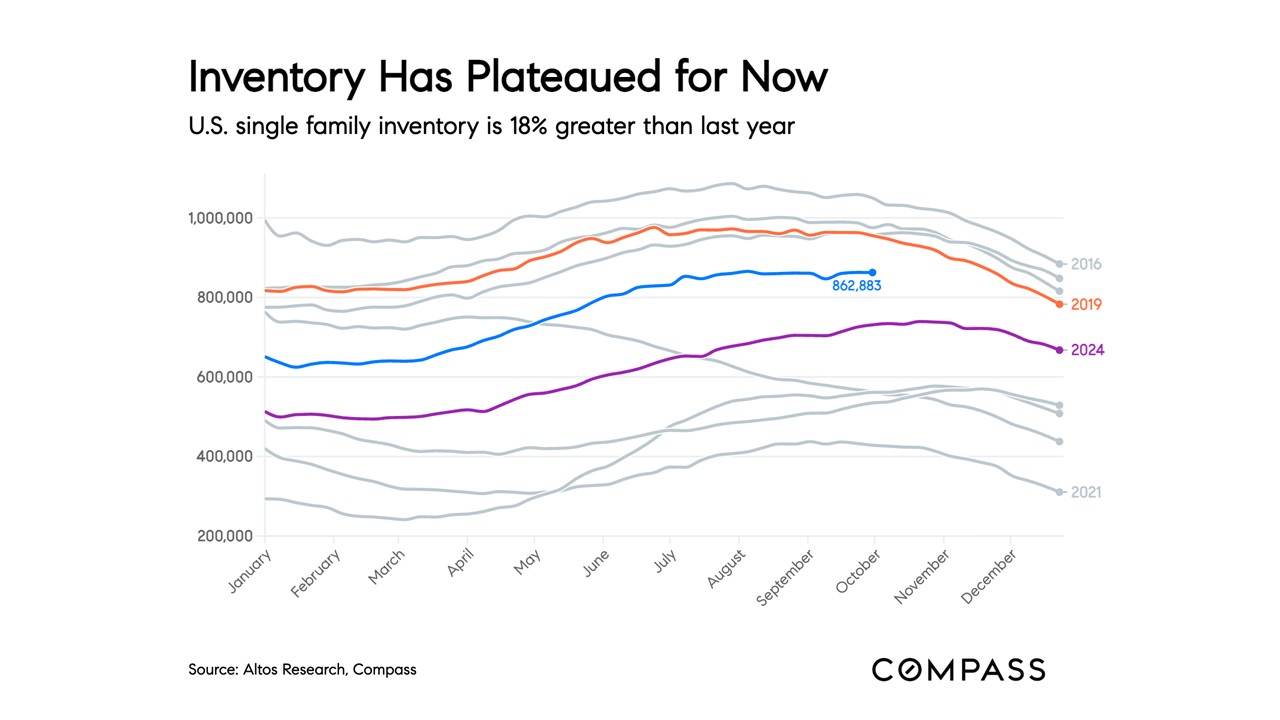

Slide 8

In one of the data visualization formats that Mike popularized through Altos research, this stacked line chart demonstrates that nationally inventory has plateaued for the year and well below 2019 and other pre-covid years. This indicates that inventory is still reasonably tight, especially in the markets with high demand despite higher interest rates.

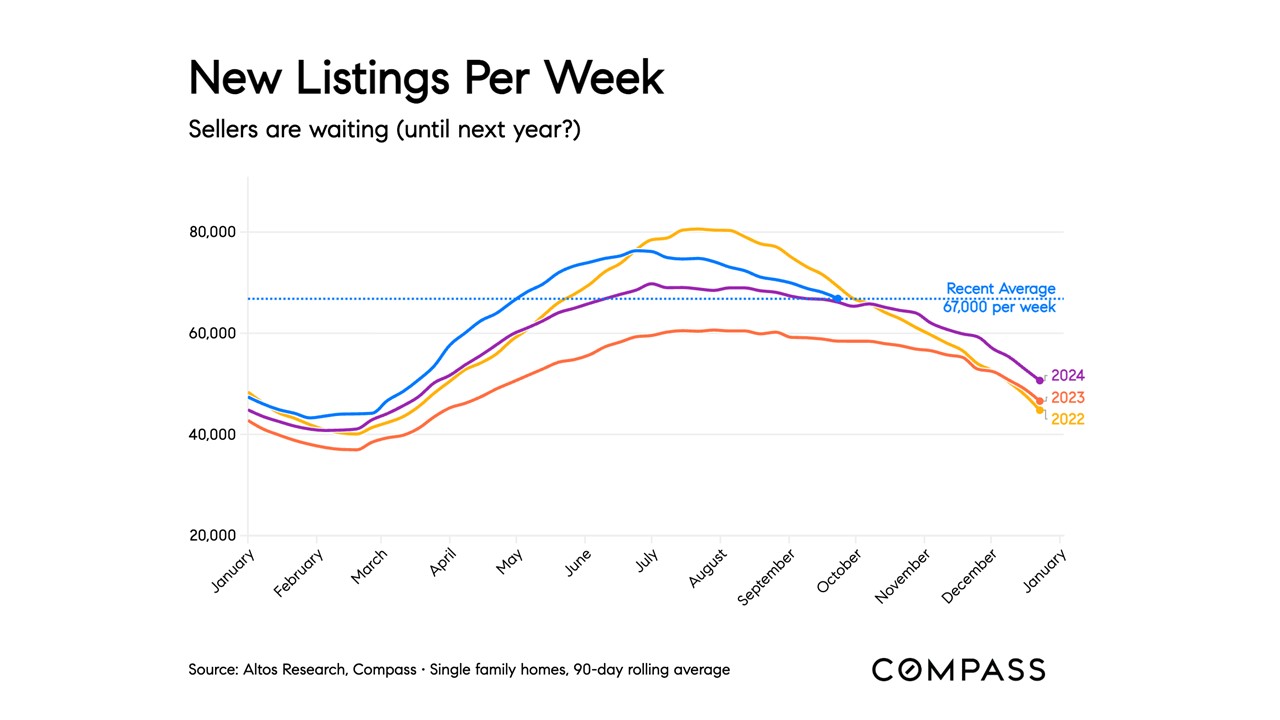

Slide 9

As Mike indicated in the chart's sub-heading, it appears as though the number of new listings has sharply declined for the year and that sellers are potentially waiting for next year, most likely when they expect interest rates to be lower. My interpretation is that this could result in one of two things happening: (1) because of such high percentage of equity and because sub-3% mortgages have principal payments exceeding the portion of interest they pay, maybe we'll have less new inventory next year, which could lead to increased home prices. Or, (2) Mike is right and the folks who would normally be selling now are waiting until next year, which could mean a surge in new listings is coming in late Q1 and Q2.

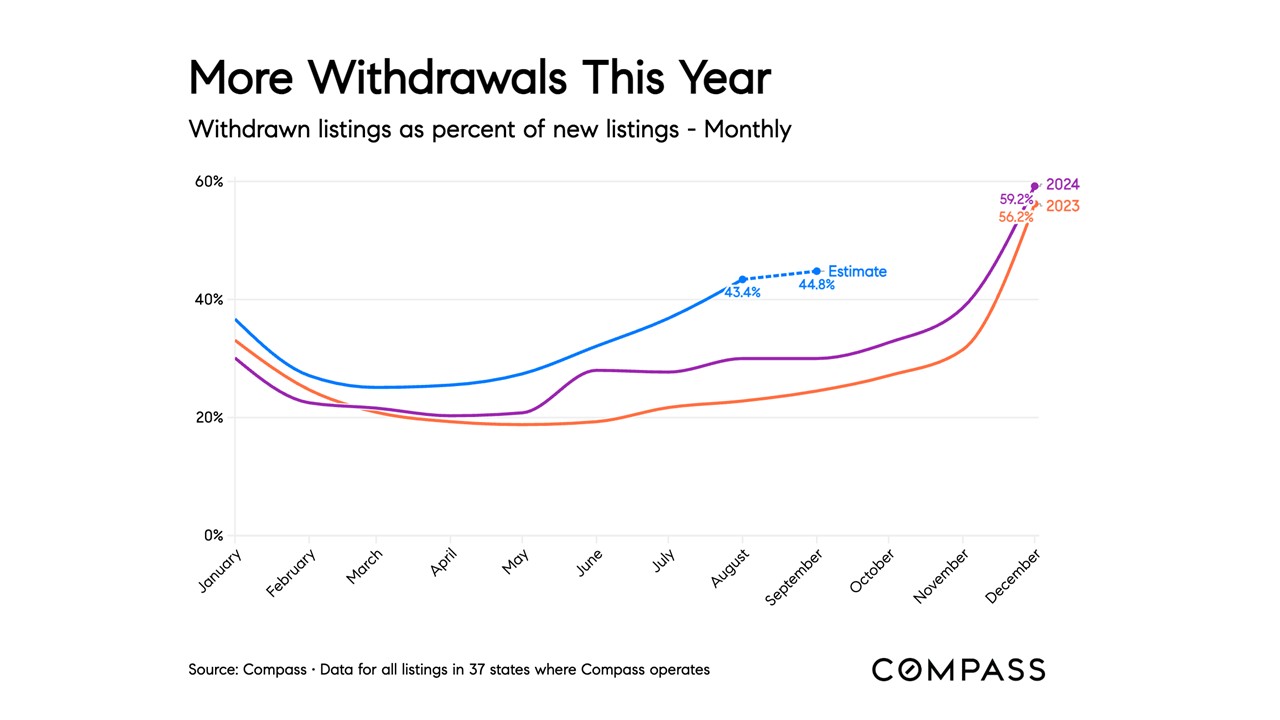

Slide 10

This slide illustrates that more sellers are pulling their homes from the market, at an earlier time of year than what normally occurs prior to the holidays. Similar to other assumptions, this could be that Sellers don't think the economic climate is strong enough right now for them to be able to maximize their selling price, therefore they are withdrawing their listings from the market. If rates fall and demand picks up, these sellers may have gambled accurately and they may be able to get their dream selling price next year. Of course, there are a lot of MAYBE's in that sentence and, alternatively, if there is a surge of new listings next year, it could put ever more downward pressure on selling prices.

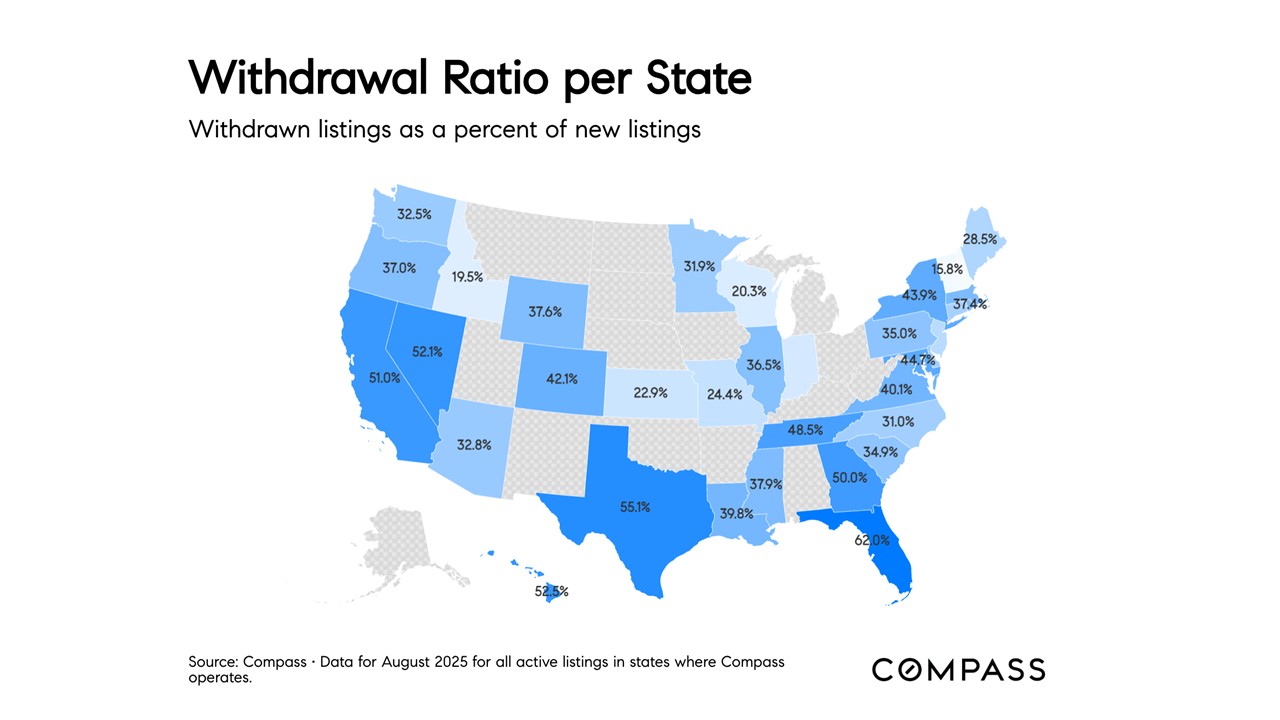

Slide 11

This heat map illustrates that states with the highest number of listing withdrawals. Understandably so, the states with the highest percentage of withdrawals are also the states with the longest average days on market and the highest number of competing listings.

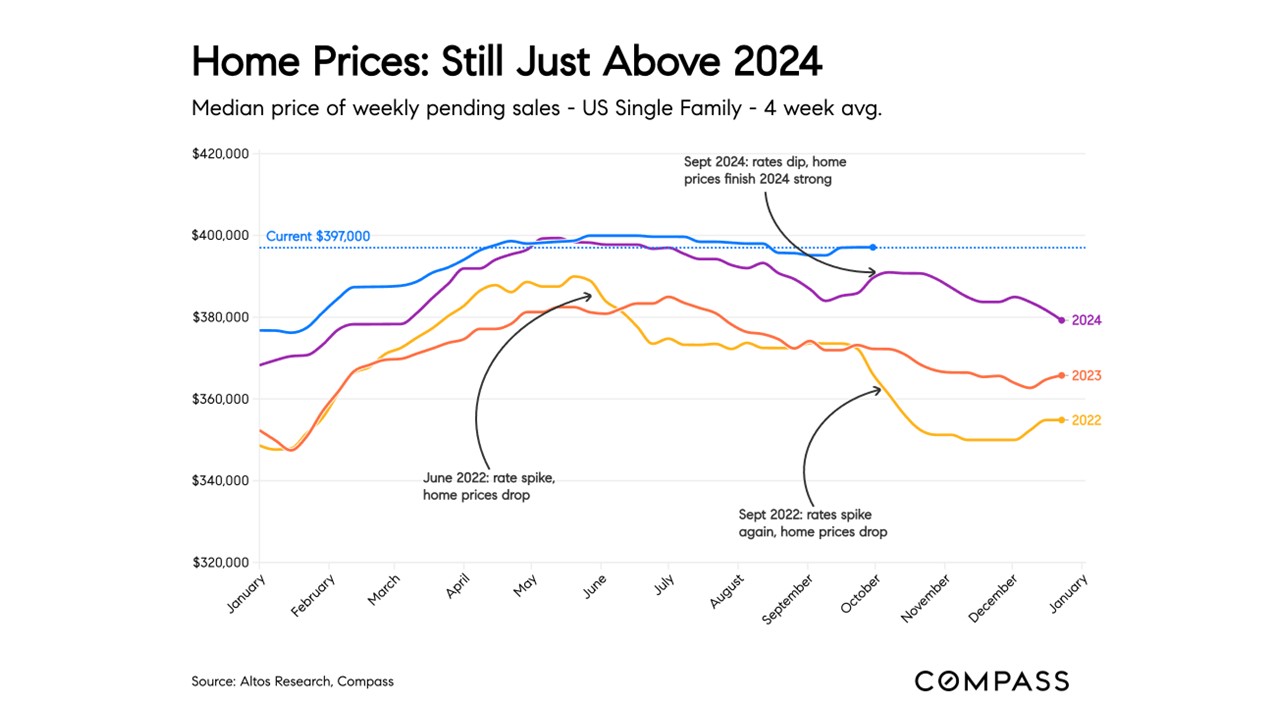

Slide 12

This is the slide to which we referenced earlier in the post. The three arrows that Mike has added to this stacked line chart illustrate that when rates spike, prices fall rather immediately. And, the converse is also true, that when rates fall, prices notably increase. This chart is effectively the answer Mike gives when people ask whether interest rates are going to increase or go down. Mike says, if rates fall below 6%, prices will most likely increase. If they approach 7%, then prices will most likely decrease.

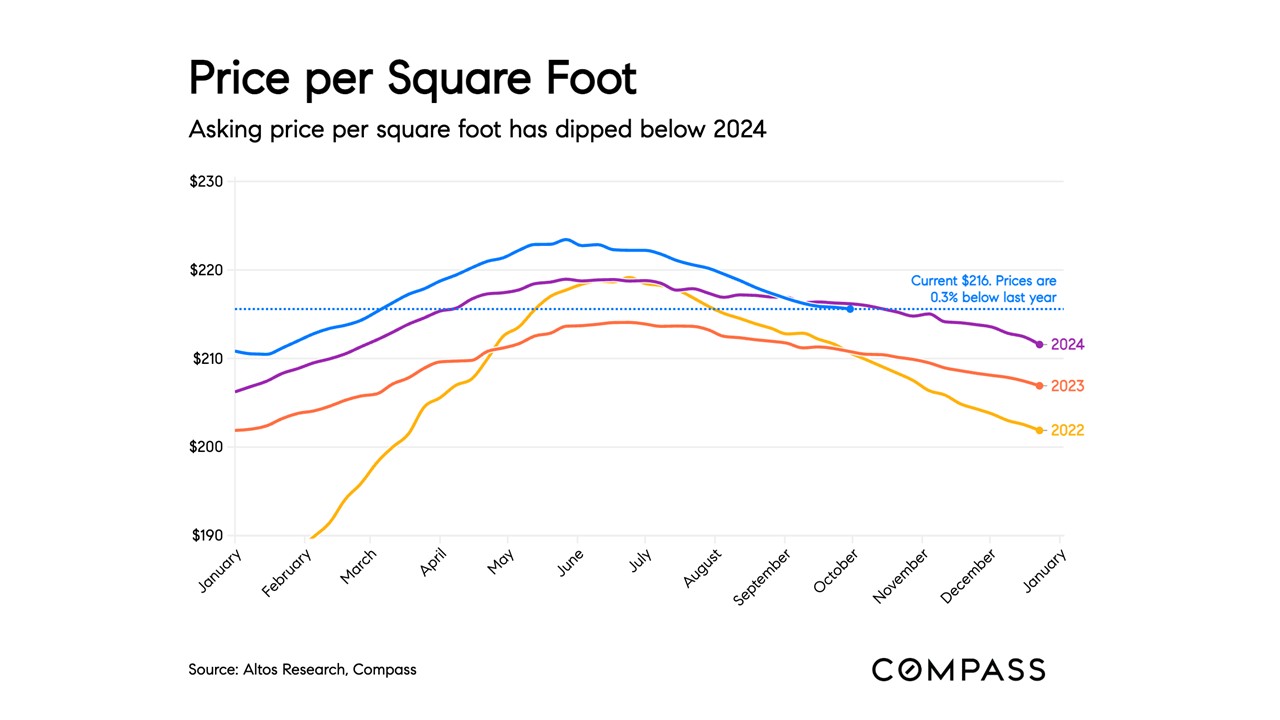

Slide 13

Although this slide indicates that price per square foot on a national basis have fallen below 2024 levels, if mortgage rates continue to trend closer to 6%, we are likely to see the 2025 price per foot inch above the 2024 level.

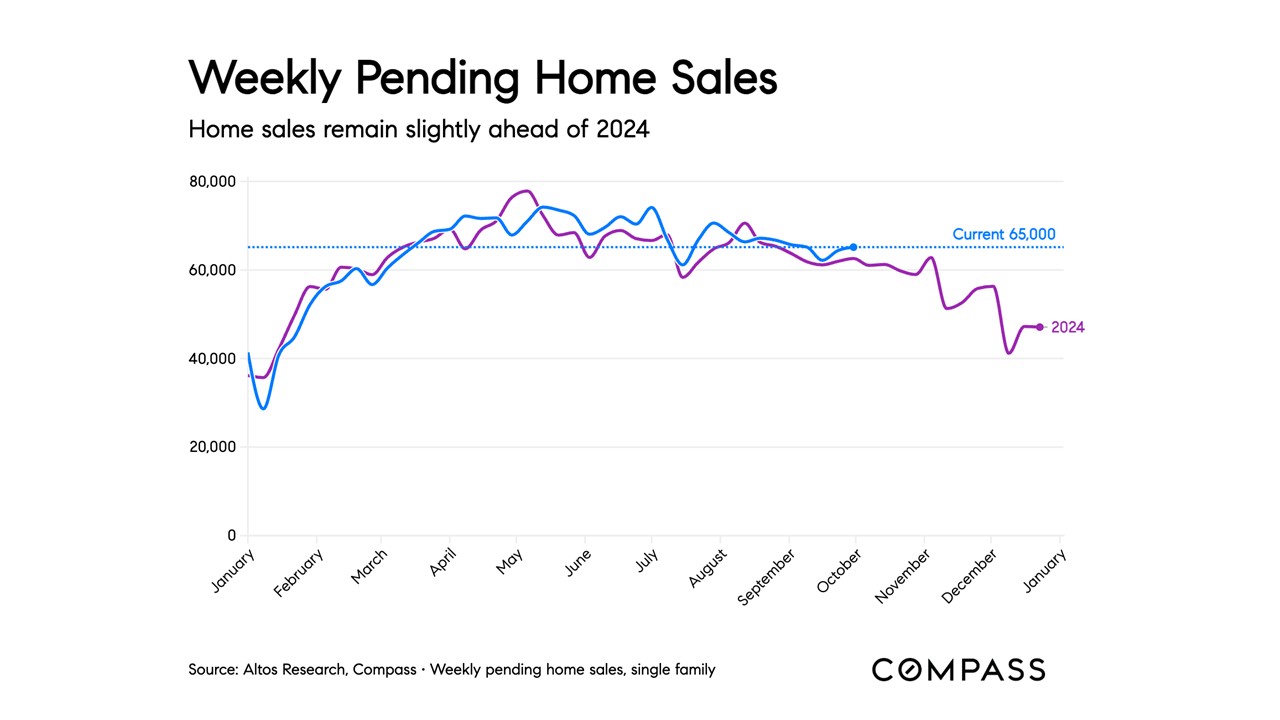

Slide 14

In the final slide of the data portion of Mike's presentation, the number of pending sales is still above 2024 levels, but not by much. This leads a lot of economists to believe that we will have approximately the same number of homes sales nationally (~4m) as we did last year, which is more than 30% below the peak selling volume during the pandemic at which time we had over 6.1m homes sold.

Slide 15

If you've enjoyed the data in these slides, we highly recommend you use the QR code to subscribe to Mike Simonsen's email newsletter in which he shares weekly videos going over the real estate data from the prior week. We've been long-time subscribers to Mike's newsletter and find his analysis to be very valuable.

Conclusion

After reflecting on the learnings we took from Mike's presentation, Alyssa and I agreed that now is an excellent time to buy real estate and hold it for the long term. Because interest rates are hovering in the mid-to-low 6's, they are still not quite low enough for prices to appreciate. Combine that with the typical slow down of transactions in Q4, sellers with homes on the market this time of year are most likely more motivated to sell than the owner who has withdrawn their listing from the market in hopes of selling it for more next year. Therefore, a purchase in Q4 offers a great opportunity to get a good purchase price, make money on the buy, then when rates fall and the availability of new homes to buy are at all time lows in the next 24 months, property values of existing homes will most likely appreciate. Of course, this is just one man's assumption of what may result if the stars align and is not financial or investment advice.

I hope you've enjoyed this recap and found it valuable context for your own purchasing and/or selling decisions.

Posted by Chris Murphy on

Leave A Comment